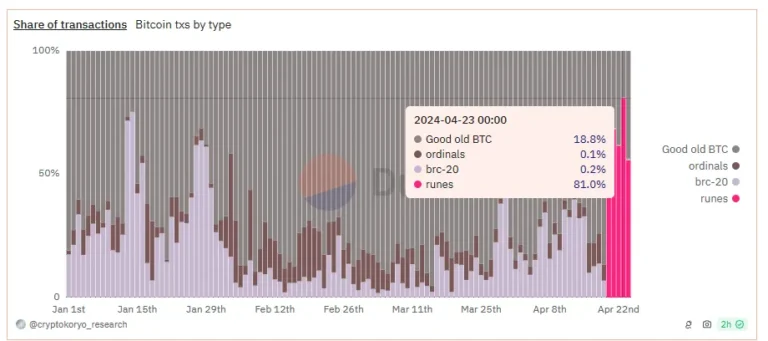

News Arts & Entertainment Art Takes Center Stage at Growing Student Protests for Palestine April 24, 2024 Automotive Rental Car Market Outlook Spans Strong Macros and Mixed Micros April 24, 2024 Books & Literature Tracie McMillan on the Myth of Colorblindness April 25, 2024 Building & Construction BAM Basements and Masons: Central Iowa’s Premier Basement Repair and Masonry Company Continues to Provide Quality Services March 26, 2024 Business Walgreens to help bring cell and gene therapies to patients as it expands specialty pharmacy services April 25, 2024 Cryptocurrency Bitcoin Runes Transactions Are Taking Over the Network—And Dominating BRC-20 April 24, 2024 Education Paraprofessional Job Description Templates and Examples April 24, 2024 Family & Parenting From One Home To The Next: How To Navigate Selling Your First Home April 25, 2024 Fashion & Beauty Beiersdorf and Rubedo join forces to target cellular senescence April 24, 2024 Finance Personal Loan Application Denied? Here’s How to Recover April 24, 2024 Foreign Language 馬來西亞南亞科技原始碼有限公司慶祝網路開發產業卓越15週年 March 11, 2024 Gov & Politics RNC Election Integrity Counsel Indicted In Arizona Fake Elector Scheme April 24, 2024 Health & Fitness Some patients who see female doctors could live longer, study suggests: ‘Higher empathy’ April 24, 2024 Home & Garden Oklahoma Foundation Solutions Offers Premium Quality Foundation Repair Services in Oklahoma City March 2, 2024 Lifestyle ‘The Bear’ Season Three Cast Some Very Familiar GQ Faces April 3, 2024 Real Estate Rocket Home Offers: Your Trusted Partner for Selling Your House Fast for Cash April 21, 2024 Religion On Volunteer Recognition Day, the Church of Scientology Nashville Thanks Volunteers Everywhere Whose Help Makes Life Better for Us All April 21, 2024 Science Climate change is bringing malaria to new areas. In Africa, it never left April 25, 2024 Sports 2024 NFL Mock Draft: Four trades concluding with a QB-needy team moving back into Round 1 April 25, 2024 Technology Zuckerberg says it will take Meta years to make money from generative AI April 24, 2024 Travel The Canary Islands are tired of the tourism model. So, they’re protesting—internationally April 22, 2024

BAM Basements and Masons: Central Iowa’s Premier Basement Repair and Masonry Company Continues to Provide Quality Services March 26, 2024

Walgreens to help bring cell and gene therapies to patients as it expands specialty pharmacy services April 25, 2024

Some patients who see female doctors could live longer, study suggests: ‘Higher empathy’ April 24, 2024

Oklahoma Foundation Solutions Offers Premium Quality Foundation Repair Services in Oklahoma City March 2, 2024

On Volunteer Recognition Day, the Church of Scientology Nashville Thanks Volunteers Everywhere Whose Help Makes Life Better for Us All April 21, 2024

2024 NFL Mock Draft: Four trades concluding with a QB-needy team moving back into Round 1 April 25, 2024

The Canary Islands are tired of the tourism model. So, they’re protesting—internationally April 22, 2024