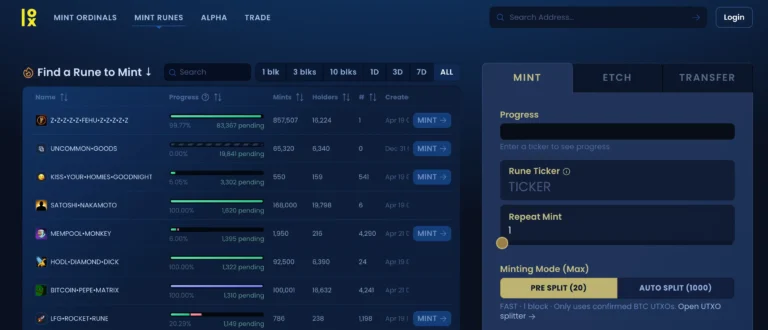

News Arts & Entertainment Art Takes Center Stage at Growing Student Protests for Palestine April 24, 2024 Automotive Rental Car Market Outlook Spans Strong Macros and Mixed Micros April 24, 2024 Books & Literature Lit Hub Daily: April 25, 2024 April 25, 2024 Building & Construction BAM Basements and Masons: Central Iowa’s Premier Basement Repair and Masonry Company Continues to Provide Quality Services March 26, 2024 Business Bristol Myers Squibb beats on revenue, launches $1.5 billion cost cuts as it posts quarterly loss April 25, 2024 Cryptocurrency How to Get Started With Bitcoin Runes: A Guide to Etching, Minting and Trading April 25, 2024 Education Paraprofessional Job Description Templates and Examples April 24, 2024 Family & Parenting From One Home To The Next: How To Navigate Selling Your First Home April 25, 2024 Fashion & Beauty Shiseido's Drunk Elephant makes Chinese retail debut at Sephora April 25, 2024 Finance How to Escape From a Money Rut April 25, 2024 Foreign Language 馬來西亞南亞科技原始碼有限公司慶祝網路開發產業卓越15週年 March 11, 2024 Gov & Politics Biden To Announce The Historic Creation Of 70,000 Good Paying Manufacturing Jobs April 25, 2024 Health & Fitness 5 women’s health tips to prevent and detect strokes, according to cardiologists April 25, 2024 Home & Garden Oklahoma Foundation Solutions Offers Premium Quality Foundation Repair Services in Oklahoma City March 2, 2024 Lifestyle ‘The Bear’ Season Three Cast Some Very Familiar GQ Faces April 3, 2024 Real Estate Rocket Home Offers: Your Trusted Partner for Selling Your House Fast for Cash April 21, 2024 Religion On Volunteer Recognition Day, the Church of Scientology Nashville Thanks Volunteers Everywhere Whose Help Makes Life Better for Us All April 21, 2024 Science The Mars Sample Return mission has a shaky future, and NASA is calling on private companies for backup April 25, 2024 Sports Knicks vs. 76ers odds, score prediction, time: 2024 NBA playoff picks, Game 3 best bets by proven model April 25, 2024 Technology Anyone want to buy TikTok? April 25, 2024 Travel The Canary Islands are tired of the tourism model. So, they’re protesting—internationally April 22, 2024

BAM Basements and Masons: Central Iowa’s Premier Basement Repair and Masonry Company Continues to Provide Quality Services March 26, 2024

Bristol Myers Squibb beats on revenue, launches $1.5 billion cost cuts as it posts quarterly loss April 25, 2024

Oklahoma Foundation Solutions Offers Premium Quality Foundation Repair Services in Oklahoma City March 2, 2024

On Volunteer Recognition Day, the Church of Scientology Nashville Thanks Volunteers Everywhere Whose Help Makes Life Better for Us All April 21, 2024

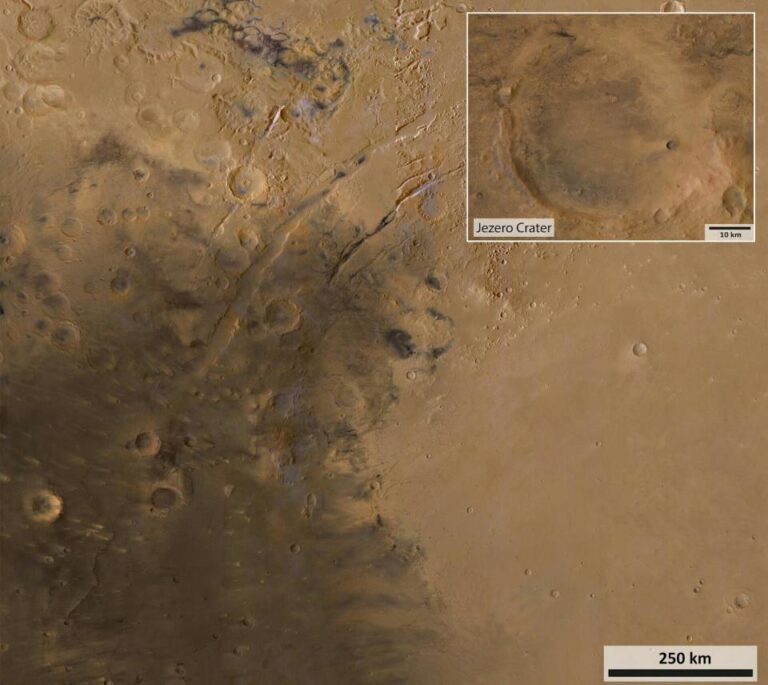

The Mars Sample Return mission has a shaky future, and NASA is calling on private companies for backup April 25, 2024

Knicks vs. 76ers odds, score prediction, time: 2024 NBA playoff picks, Game 3 best bets by proven model April 25, 2024

The Canary Islands are tired of the tourism model. So, they’re protesting—internationally April 22, 2024